The euro area inflation outlook: a scenario analysis

Lecture by Isabel Schnabel, Member of the Executive Board of the ECB, at the Ragnar Nurkse Lecture Series organised by Eesti Pank in Tallinn, Estonia

Tallinn, 30 August 2024

Disinflation in the euro area has proceeded rapidly. Headline inflation fell from a peak of 10.6% in October 2022 to 2.6% in July of this year. Data released yesterday suggest that in August inflation has declined further in parts of the euro area.

These are welcome developments. They largely reflect an unwinding of the forces that over the past three years have led to strong increases in the prices of energy, food and goods, as well as the impact of our restrictive monetary policy.

However, the current level of headline inflation understates the challenges monetary policy is still facing. In particular, domestic inflation remains high at 4.4%, largely reflecting persistent price pressures in the services sector, where disinflation has effectively stalled since last November.

While goods inflation has fallen back to its pre-pandemic average at a fast pace, services inflation is still more than twice as high as its average between 1999 and 2019 (Slide 2, left-hand chart).

As a result, services have accounted, on average, for 70% of headline inflation since the start of the year (Slide 2, right-hand chart). Within the services sector, price pressures are broad-based, with strong wage growth being just one factor keeping inflation at elevated levels (Slide 3, left-hand chart).

Stubbornly high price pressures in the services sector are a global phenomenon. Across many advanced economies, services inflation remains high, even if there has been, on average, more progress towards pre-pandemic levels than in the euro area (Slide 3, right-hand chart).

Continued high inflation momentum, defined as the annualised three-month-on-three-month change, suggests that services prices keep rising at an elevated pace of almost 5% (Slide 4, left-hand side).

Medium-term price stability does not require services inflation to slow to 2%. Persistent relative price changes, often reflecting sectoral differences in productivity growth, are not unusual. In many advanced economies, the prices of services relative to those of goods have increased for a long time (Slide 4, right-hand side).

But for price stability to be restored sustainably, services inflation needs to return to a level that is consistent with underlying inflation of 2% over the medium term.

Uncertainty calls for policy robustness

To assess whether the current monetary and financial conditions will secure a timely return of inflation to target, policymakers need to take a stand on the likely future evolution of the economy.

Incoming data offer useful clues in this regard. But since monetary policy affects the economy with long and variable lags, there is a risk that policy might be adjusted too slowly if too much weight is given to backward-looking data.

Therefore, economic projections remain a key input to our decision-making process.

In the euro area, the latest Eurosystem staff projections are consistent with a return to price stability. They predict that inflation will fall to 2.2% in 2025 and to 1.9% in 2026, even if the last mile of disinflation is expected to be bumpy, with inflation likely to fall in the coming months before rising again towards the end of the year.

Under strict inflation forecast targeting, policy should be adjusted to validate the financial conditions on which this outlook relies.

However, inflation forecast targeting was already a challenge even in more tranquil times when shocks to inflation and its drivers were less pervasive.[1]

Since 2001, inflation projections from the forecasting community, including the ECB, have on average had little explanatory power for realised inflation over horizons beyond the very short term (Slide 5).[2] In most cases, these forecasts almost mechanically converge to the 2% target, unless judgement is applied.

Managing inflation is particularly challenging in an era of transformation.[3]

We are seeing fundamental changes in labour and energy markets and a reorganisation of global supply chains. At the same time, due to structural headwinds in some euro area economies, it is increasingly difficult to identify the impact of monetary policy on growth and inflation.

These forces make it inherently more complex to produce accurate projections even over shorter horizons. While short-term forecast errors for inflation have generally come down since the start of the year, this masks differences within the Harmonised Index of Consumer Prices (HICP) basket.

In particular, recent improved forecast accuracy for core inflation reflects offsetting forecast errors for goods and services. Since January, disinflation in services has consistently been slower than anticipated.

In this environment, policy should be robust to contingencies causing the economy to evolve differently from what is implied by the modal outlook. Monetary policy that would be optimal under strict inflation forecast targeting can be suboptimal when knowledge is imperfect.[4]

Monetary policy to remain focused on bringing inflation down

Scenario analysis is a powerful tool for making policy more robust while retaining a forward-looking perspective. Plausible alternative scenarios that scrutinise the key assumptions underlying the modal outlook highlight the large uncertainty surrounding the baseline scenario.

If this uncertainty is communicated clearly and transparently, the distribution of future expected policy outcomes may better reflect the risks to the modal outlook.

Inevitably, policy cannot be robust to all contingencies. A policy that is robust to downside risks is unlikely to be equally resilient against upside risks, and vice versa. Central banks thus need to weigh the risks and focus on those considered to be the most detrimental to the achievement of their mandate.

In the current environment, monetary policy should remain focused on bringing inflation back to our target in a timely manner, for three main reasons.

First, while risks to growth have increased, a soft landing still looks more likely than a recession.

In recent weeks, financial markets have repriced more fundamentally the expected pace of central bank easing, also in the euro area. This reflects concerns that global growth is at risk of a rapid deterioration.

While growth prospects warrant close scrutiny in the coming weeks, the market repricing reflects, by and large, spillovers from abroad that were amplified by technical factors, including reduced liquidity during the summer period and the unwinding of yen carry trades.

It is therefore unclear to what extent the repricing reflects a change in macroeconomic fundamentals, also given the relative stability of growth forecasts for major economies by market analysts (Slide 6). At the ECB, too, growth projections for the euro area for 2024 and 2025 have remained broadly stable since September 2023.

While monetary policy has to avoid unnecessary pain, it must also avoid overreacting to volatile financial market expectations. Central banks’ actions should be guided by their evolving assessment of the inflation and growth outlook.

Second, history shows that central banks were often unsuccessful in bringing inflation back to target after a long period of very high inflation.[5]

In their new research, Christina and David Romer show that perseverance is critical for successfully restoring price stability after a large inflation shock.[6] They demonstrate that strong perceived commitment to disinflation has often not been sufficient to reduce inflation through its impact on expected inflation.

Rather, successful disinflation was typically the result of policymakers having persisted in their efforts to fully extinguish past inflationary shocks.[7] Hence, central banks must not abandon disinflationary policies too early.

In the euro area, as we gained confidence in the projected disinflation path, we decided to start dialling back the degree of policy restraint earlier than central banks in other advanced economies. But the earlier monetary policy shifts in response to forward-looking signals, the more cautious and gradual it can afford to be on the way back to (an unknown) neutral.

Third, even if inflation is no longer a primary concern to financial markets, it is still very much on people’s minds.

Although headline inflation has come down quickly, inflation perceptions are proving more persistent, and untypically so from a historical perspective. Today, more than 40% of people still regard inflation as having risen “a lot” over the past 12 months (Slide 7, left-hand side).

Elevated inflation perceptions raise inflation persistence and make inflation expectations more susceptible to new shocks, as memory cues make people recall past inflation experiences more rapidly.[8]

In a new study, economists at the Federal Reserve Board quantify these risks.[9] They show that inflation persistence has increased measurably across advanced economies, including the euro area.

As a result, if today the euro area were to be hit by a “normal” supply shock, as opposed to the unusually large shocks of the past few years, inflation would be higher by almost one percentage point next year compared with a scenario where inflation persistence is lower.

This risk is also reflected in the right tail of the inflation expectations distribution remaining thicker than before the pandemic, even among professional forecasters (Slide 7, right-hand side).

Incoming data broadly confirm the baseline scenario

Making policy robust to these risks requires a thorough review of the main assumptions underlying the baseline scenario for policy to be adjusted. Such a broad-based review is carried out every three months when the projections are updated.

In the euro area, the expected decline in headline inflation to the 2% target by the end of 2025 rests on three critical assumptions.

One is that the current high growth in unit labour costs predominantly reflects the lagged effects of past price shocks related to the pandemic and Russia’s invasion of Ukraine.

As many wage contracts are only infrequently negotiated, the economy can take some time to return to equilibrium. The recent sharp decline in headline inflation should therefore progressively lead to lower wage growth, as also suggested by staff analysis (Slide 8, left-hand side).

Unit labour cost growth is expected to slow further once the adverse impact of labour hoarding on productivity growth reverses as demand recovers.

The second assumption is that firms are absorbing a large part of the current strong increases in unit labour costs in their profit margins, as the current level of interest rates is dampening the growth in aggregate demand.

The third assumption is that price pressures outside the services sector will ease further or evolve in line with historical regularities.

Over recent weeks, incoming data have lent support to these assumptions.

Negotiated wage growth slowed visibly in the second quarter. Although part of this development is driven by volatile one-off payments, with wage growth expected to reaccelerate in the third quarter, surveys and private sector forecasts suggest that expected wage increases will moderate measurably in 2025 and beyond (Slide 8, right-hand side).

Firms also expect that increases in their selling prices will decline as growth in input costs slows.

According to the most recent Survey on Access to Finance of Enterprises (SAFE), selling prices are expected to increase by 3% on average over the next 12 months, down from 4.5% at the end of last year (Slide 9, left-hand chart). While firms in the services sector still expect a larger increase in their selling prices compared with other sectors, the size of intended price increases is declining there too.

Firms have also started to use their margins to absorb the increases in labour costs. In the first quarter of this year, unit profits no longer contributed to inflation in a meaningful way (Slide 9, right-hand chart). This is a significant change from last year.

Monetary policy is actively supporting this rebalancing process. By constraining growth in aggregate demand, it makes it more difficult for firms to pass on higher costs to consumers. Surveys suggest that the current level of interest rates is incentivising people to save more and spend less.

Notably, savings intentions for the coming year have never been higher than they are today, with households actively shifting their savings into time deposits offering higher returns (Slide 10). As consumer confidence is recovering and households’ unemployment expectations remain subdued, it is likely that the desire to save is not driven by precautionary motives only.

Finally, energy and food inflation have recently surprised to the downside, while a stronger euro, coupled with the recent fall in oil prices, can ease headline inflation further, at least over the near term.

All in all, recent data remain consistent with the baseline scenario that foresees that inflation will sustainably fall back to our 2% target by the end of 2025. Along with signs of a potential decline in economic momentum in other parts of the world, there is less risk that a further moderate and gradual dialling back of policy restraint could derail the path back to price stability.

An alternative scenario: scrutinising the key assumptions

It is conceivable, however, that the conditions on which the modal outlook rests do not materialise. Scenario analysis can reveal the reasoning behind these risks and evaluate their consequences for the inflation outlook.

Unit labour cost growth could remain high for longer

In the alternative scenario, growth in unit labour costs would not come down as quickly as projected. In the June Eurosystem staff projections, annual growth in unit labour costs is expected to fall to 2.5% in 2025, from 4.7% this year.

This is a sharp decline, especially as unit labour costs were still growing at an annual rate of 5.3% in the first quarter, with momentum remaining high. By way of comparison, annual unit labour cost growth in the United States was only 0.9% in the second quarter.

Growth in unit labour costs could disappoint expectations because of stronger wage growth. Although surveys suggest weaker wage growth ahead, the staggered nature of wage negotiations implies that workers may take longer than projected to recoup their purchasing power.

While in some countries, such as Portugal and Spain, workers have, on average, recouped the losses incurred in their real wages since before the pandemic, there is still a considerable share of workers in Italy, Germany, Finland and other countries whose real wages remain well below pre-pandemic levels (Slide 11). This also reflects differences in the duration of collective wage agreements.

Wages could also expand more strongly if labour market conditions remain tight. A protracted imbalance between labour supply and demand could more fundamentally challenge the assumption underlying the Eurosystem staff projections that wage growth merely reflects past price shocks and the resulting catch-up process.

While labour demand is slowing, it remains high in an environment in which unemployment is historically low and where a significant share of firms, especially in the services sector, still regards labour as a factor limiting business (Slide 12). If a shortage of labour prevents firms from increasing production, rising demand results in higher inflation rather than higher output.

Another reason why unit labour cost growth could remain higher than projected is a weaker recovery in productivity growth. In the Eurosystem projections, annual productivity growth is forecast to recover to 1% in 2025 and 1.1% in 2026, nearly double the historical average.

The pick-up in productivity growth may be weaker if part of the current weakness is not cyclical but more persistent, reflecting the structural challenges facing the euro area economy.[10] In fact, over the past year, the recovery in productivity growth has repeatedly been slower than expected.

Increasing trade tensions, environmental policies or higher energy prices could all weigh on productivity growth over the coming years, reinforcing upward pressure on the growth of unit labour costs and thus inflation.

Wage pass-through may be stronger

In addition, under the alternative scenario, firms may decide to pass on a higher-than-expected share of rising labour costs to consumers.

The Eurosystem staff projections expect unit profits to stagnate this year as firms use their margins to absorb strong growth in input costs. The buffer provided by profit margins is particularly important in the services sector, which is more labour-intensive and where inflation is still high.

New evidence for the euro area suggests, however, that the pass-through of higher wages into producer prices is typically very strong in the services sector.[11] After two and a half years, the estimated pass-through is 86%, twice as high as in the manufacturing sector (Slide 13).[12]

In other words, if the pass-through in earlier stages of the pricing chain remains as in the past, there needs to be a strong decline in profit margins for the baseline to materialise.

Softening demand for services as part of a rotation back to goods could be one such factor. So far, however, demand for services has remained relatively resilient, even if there are signs of a weakening (Slide 14).

Looking ahead, it will be critical to observe how the interplay of rising real wages, a resilient labour market and the fading impact of monetary policy tightening will contribute to aggregate demand.

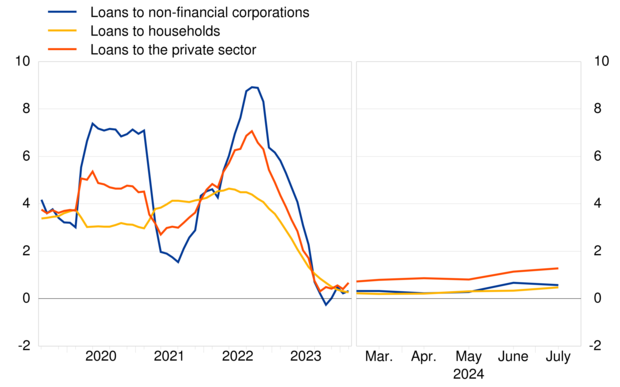

In particular, the most recent bank lending survey suggests that the economy is starting to adapt to higher interest rates, as banks reported a first increase in loan demand by households in two years, while loan demand by firms is still contracting, but at a more moderate pace (Slide 15).

Geopolitical uncertainty and protectionism pose risks to baseline

Finally, price pressures outside the services sector may reappear.

Goods inflation is a case in point. Under the baseline scenario, it is expected to remain close to current levels as the disinflationary effect of the easing in supply chain disruptions fades.

At the same time, protectionism and geopolitical uncertainty are rising. According to the Peace Research Institute Oslo, the number of state-based conflicts is the highest since 1946.[13]

Geopolitical uncertainty is a key risk for the stability of global supply chains and commodity prices. Recently, for example, container freight rates have increased measurably, in part reflecting disruptions in the Suez Canal (Slide 16). A further escalation in the Middle East could disrupt energy markets and supply chains more fundamentally.

Global trade measures are increasing in parallel, especially for critical raw materials – the production of which is often concentrated in just a few countries (Slide 17).

Together with the growing impact of climate change on food prices, these are important forces that could challenge the assumptions underlying the baseline scenario.

Conclusion

I would like to conclude with three implications for monetary policy.

First, incoming data have broadly confirmed the baseline outlook, bolstering our confidence that conditions remain in place for inflation to fall back to our 2% target by the end of 2025.

Second, confidence is not knowledge. History will not judge our intentions but our success in delivering on our mandate. Given that the path back to price stability hinges on a set of critical assumptions, policy should proceed gradually and cautiously.

In particular, the closer policy rates get to the upper band of estimates of the neutral rate of interest – that is, the less certain we are how restrictive our policy is –, the more cautious we should be to avoid that policy itself becomes a factor slowing down disinflation.

In other words, the pace of policy easing cannot be mechanical. It needs to rest on data and analysis.

Third, the world around us is changing rapidly. When the future is as uncertain as it is today, the modal outlook provides a false sense of comfort. Scenario analysis can protect us from falling victim to model uncertainty and overconfidence.

Being transparent about what could go wrong, and factoring this into the decision-making process, can help make policy more robust to contingencies that threaten the achievement of our primary mandate.

Thank you.

First, please LoginComment After ~